Inference¶

%matplotlib inline

from IPython.display import Image

import pandas

import numpy as np

import seaborn as sns

import matplotlib.pyplot as plt

import statsmodels.formula.api as sm

from sklearn.preprocessing import scale

from sklearn import metrics

Assuming you have the file downloaded on the path ../data/:

db = pandas.read_csv("../data/paris_abb.csv.zip")

If you’re online, you can do:

db = pandas.read_csv("https://github.com/darribas/data_science_studio/raw/master/content/data/paris_abb.csv.zip")

db['l_price'] = np.log1p(db['Price'])

db.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 50280 entries, 0 to 50279

Data columns (total 11 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 id 50280 non-null int64

1 neighbourhood_cleansed 50280 non-null object

2 property_type 50280 non-null object

3 room_type 50280 non-null object

4 accommodates 50280 non-null int64

5 bathrooms 50280 non-null float64

6 bedrooms 50280 non-null float64

7 beds 50280 non-null float64

8 bed_type 50280 non-null object

9 Price 50280 non-null float64

10 l_price 50280 non-null float64

dtypes: float64(5), int64(2), object(4)

memory usage: 4.2+ MB

Baseline model¶

\(X\):

Bathrooms

Bedrooms

Beds

Room type

m1 = sm.ols('l_price ~ bedrooms + bathrooms + beds', db).fit()

m1.summary()

| Dep. Variable: | l_price | R-squared: | 0.245 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.245 |

| Method: | Least Squares | F-statistic: | 5433. |

| Date: | Thu, 07 Jan 2021 | Prob (F-statistic): | 0.00 |

| Time: | 17:25:24 | Log-Likelihood: | -38592. |

| No. Observations: | 50280 | AIC: | 7.719e+04 |

| Df Residuals: | 50276 | BIC: | 7.723e+04 |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 4.1806 | 0.005 | 852.126 | 0.000 | 4.171 | 4.190 |

| bedrooms | 0.2253 | 0.004 | 57.760 | 0.000 | 0.218 | 0.233 |

| bathrooms | -0.1544 | 0.005 | -32.373 | 0.000 | -0.164 | -0.145 |

| beds | 0.1398 | 0.003 | 50.554 | 0.000 | 0.134 | 0.145 |

| Omnibus: | 11384.882 | Durbin-Watson: | 1.846 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 585415.122 |

| Skew: | -0.096 | Prob(JB): | 0.00 |

| Kurtosis: | 19.715 | Cond. No. | 7.94 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

To note:

Decent \(R^2\) (although that’s not holy truth)

Every variable significant and related as expected

Interpret coefficients

cols = ['bedrooms', 'bathrooms', 'beds']

scX = pandas.DataFrame(scale(db[cols]),

index=db.index,

columns=cols)

scX.describe()

| bedrooms | bathrooms | beds | |

|---|---|---|---|

| count | 5.028000e+04 | 5.028000e+04 | 5.028000e+04 |

| mean | 1.748138e-14 | 1.621070e-15 | -5.895298e-15 |

| std | 1.000010e+00 | 1.000010e+00 | 1.000010e+00 |

| min | -1.076738e+00 | -1.625116e+00 | -1.429042e+00 |

| 25% | -7.772733e-02 | -1.702805e-01 | -5.706025e-01 |

| 50% | -7.772733e-02 | -1.702805e-01 | -5.706025e-01 |

| 75% | -7.772733e-02 | -1.702805e-01 | 2.878366e-01 |

| max | 4.887380e+01 | 7.111664e+01 | 4.149292e+01 |

m2 = sm.ols('l_price ~ bedrooms + bathrooms + beds',

data=scX.join(db['l_price']))\

.fit()

m2.summary()

| Dep. Variable: | l_price | R-squared: | 0.245 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.245 |

| Method: | Least Squares | F-statistic: | 5433. |

| Date: | Thu, 07 Jan 2021 | Prob (F-statistic): | 0.00 |

| Time: | 17:25:24 | Log-Likelihood: | -38592. |

| No. Observations: | 50280 | AIC: | 7.719e+04 |

| Df Residuals: | 50276 | BIC: | 7.723e+04 |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 4.4837 | 0.002 | 1928.462 | 0.000 | 4.479 | 4.488 |

| bedrooms | 0.2255 | 0.004 | 57.760 | 0.000 | 0.218 | 0.233 |

| bathrooms | -0.1061 | 0.003 | -32.373 | 0.000 | -0.113 | -0.100 |

| beds | 0.1628 | 0.003 | 50.554 | 0.000 | 0.156 | 0.169 |

| Omnibus: | 11384.882 | Durbin-Watson: | 1.846 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 585415.122 |

| Skew: | -0.096 | Prob(JB): | 0.00 |

| Kurtosis: | 19.715 | Cond. No. | 3.11 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Let’s bring both sets of results together:

pandas.DataFrame({"Baseline": m1.params,

"X Std.": m2.params

})

| Baseline | X Std. | |

|---|---|---|

| Intercept | 4.180599 | 4.483657 |

| bedrooms | 0.225325 | 0.225548 |

| bathrooms | -0.154385 | -0.106119 |

| beds | 0.139759 | 0.162806 |

To note:

How does interpretation of the coefficients change?

Meaning of intecept when \(X\) is demeanded

Units in which \(\beta\) are interpreted

Predictive checking¶

Is the model picking up the overall “shape of data”?

Important to know how much we should trust our inferences

Crucial if we want to use the model to predict!

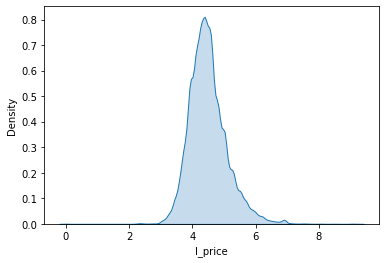

sns.kdeplot(db['l_price'], shade=True)

<AxesSubplot:xlabel='l_price', ylabel='Density'>

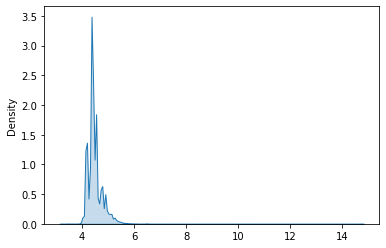

sns.kdeplot(m1.fittedvalues, shade=True)

<AxesSubplot:ylabel='Density'>

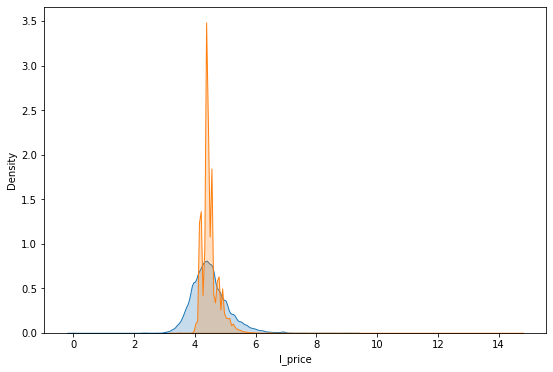

f, ax = plt.subplots(1, figsize=(9, 6))

sns.kdeplot(db['l_price'], shade=True, ax=ax, label='$y$')

sns.kdeplot(m1.fittedvalues, shade=True, ax=ax, label='$\hat{y}$')

plt.show()

To note:

Not a terrible start

How could we improve it?

m3 = sm.ols('l_price ~ bedrooms + bathrooms + beds + room_type', db).fit()

m3.summary()

| Dep. Variable: | l_price | R-squared: | 0.340 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.340 |

| Method: | Least Squares | F-statistic: | 4314. |

| Date: | Thu, 07 Jan 2021 | Prob (F-statistic): | 0.00 |

| Time: | 17:25:25 | Log-Likelihood: | -35210. |

| No. Observations: | 50280 | AIC: | 7.043e+04 |

| Df Residuals: | 50273 | BIC: | 7.050e+04 |

| Df Model: | 6 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 4.2417 | 0.005 | 899.941 | 0.000 | 4.232 | 4.251 |

| room_type[T.Hotel room] | 0.5548 | 0.016 | 35.619 | 0.000 | 0.524 | 0.585 |

| room_type[T.Private room] | -0.4862 | 0.007 | -66.604 | 0.000 | -0.501 | -0.472 |

| room_type[T.Shared room] | -1.0320 | 0.028 | -36.320 | 0.000 | -1.088 | -0.976 |

| bedrooms | 0.2388 | 0.004 | 65.134 | 0.000 | 0.232 | 0.246 |

| bathrooms | -0.1440 | 0.004 | -32.285 | 0.000 | -0.153 | -0.135 |

| beds | 0.1144 | 0.003 | 43.386 | 0.000 | 0.109 | 0.120 |

| Omnibus: | 11695.728 | Durbin-Watson: | 1.878 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 680804.847 |

| Skew: | -0.027 | Prob(JB): | 0.00 |

| Kurtosis: | 21.027 | Cond. No. | 37.2 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

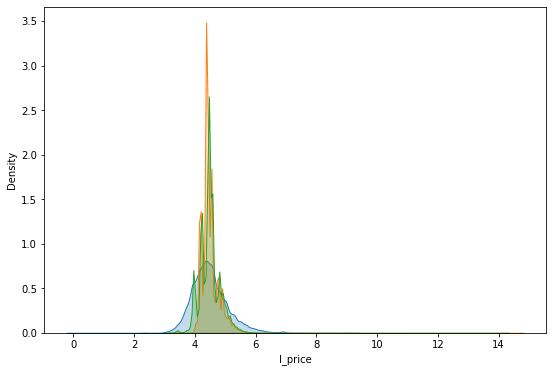

f, ax = plt.subplots(1, figsize=(9, 6))

sns.kdeplot(db['l_price'], shade=True, ax=ax, label='$y$')

sns.kdeplot(m1.fittedvalues, shade=True, ax=ax, label='$\hat{y}_1$')

sns.kdeplot(m3.fittedvalues, shade=True, ax=ax, label='$\hat{y}_2$')

plt.show()

To note:

This is better!

But these are only point predictions. Sometimes that’s good enough.

Usually however, we want a model to capture the underlying process instead of the particular realisation observed (ie. dataset).

Then we need to think about the uncertainty embedded in the model we are estimating

Inferential Vs Predictive uncertainty¶

[See more in Chapter 7.2 of Gelman & Hill 2006 👌💯]

Two types of uncertainty in our model

Predictive (\(\epsilon\))

Inferential (\(\beta\))

Both affect the final predictions we make

Image("../figs/abb_room.png", retina=True)

room = db.loc[db['id']==35607436, :]

room.T

| 45979 | |

|---|---|

| id | 35607436 |

| neighbourhood_cleansed | Luxembourg |

| property_type | Apartment |

| room_type | Entire home/apt |

| accommodates | 5 |

| bathrooms | 1 |

| bedrooms | 2 |

| beds | 3 |

| bed_type | Real Bed |

| Price | 90 |

| l_price | 4.51086 |

rid = room.index[0]

db.loc[rid, :]

id 35607436

neighbourhood_cleansed Luxembourg

property_type Apartment

room_type Entire home/apt

accommodates 5

bathrooms 1

bedrooms 2

beds 3

bed_type Real Bed

Price 90

l_price 4.51086

Name: 45979, dtype: object

m1.params['Intercept'] + db.loc[rid, cols].dot(m1.params[cols])

4.896141184855212

To note:

What does

dotdo?

m1.fittedvalues[rid]

4.896141184855212

Point predictive simulation¶

%%time

# Parameters

## Number of simulations

r = 2000

# Pull out characteristics for house of interest

x_i = db.loc[rid, cols]

# Specify model engine

model = m1

# Place-holder

sims = np.zeros(r)

# Loop over number of replications

for i in range(r):

# Get a random draw of betas

rbs = np.random.normal(model.params, model.bse)

# Get a random draw of epsilon

re = np.random.normal(0, model.scale)

# Obtain point estimate

y_hr = rbs[0] + np.dot(x_i, rbs[1:]) + re

# Store estimate

sims[i] = y_hr

CPU times: user 637 ms, sys: 35.1 ms, total: 672 ms

Wall time: 632 ms

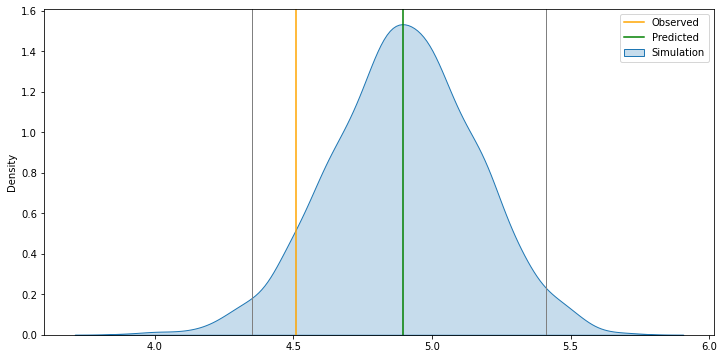

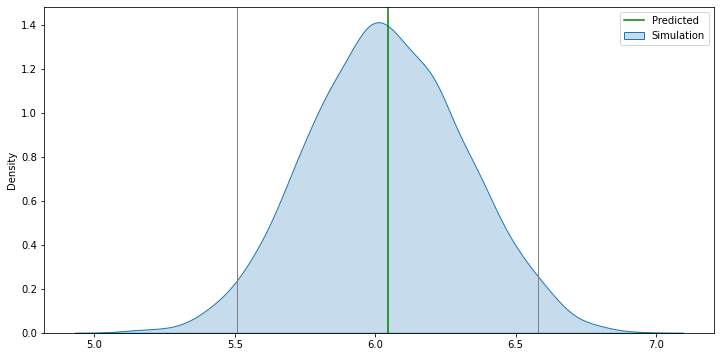

f, ax = plt.subplots(1, figsize=(12, 6))

sns.kdeplot(sims, shade=True, ax=ax, label='Simulation')

ax.axvline(db.loc[rid, 'l_price'], c='orange', label='Observed')

ax.axvline(model.fittedvalues[rid], c='green', label='Predicted')

lo, up = pandas.Series(sims)\

.sort_values()\

.iloc[[int(np.round(0.025 * r)), int(np.round(0.975 * r))]]

ax.axvline(lo, c='grey', linewidth=1)

ax.axvline(up, c='grey', linewidth=1)

plt.legend()

plt.show()

To note:

Intuition of the simulation

The

forloop, deconstructedThe graph, bit by bit

If we did this for every observation, we’d expect 95% to be within the 95% bands

Exercise

Explore with the code above and try to generate similar plots for:

Different houses across locations and characteristics

Different model

Exercise+

Recreate the analysis above for observation 5389821. What happens? Why?

Now, we could do this for all the observations and get a sense of the overall distribution to be expected

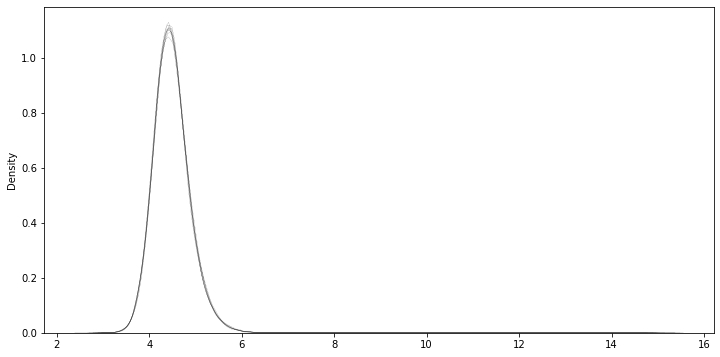

%%time

# Parameters

## Number of observations & simulations

n = db.shape[0]

r = 200

# Specify model engine

model = m1

# Place-holder (N, r)

sims = np.zeros((n, r))

# Loop over number of replications

for i in range(r):

# Get a random draw of betas

rbs = np.random.normal(model.params, model.bse)

# Get a random draw of epsilon

re = np.random.normal([0]*n, model.scale)

# Obtain point estimate

y_hr = rbs[0] + np.dot(db[cols], rbs[1:]) + re

# Store estimate

sims[:, i] = y_hr

CPU times: user 5.61 s, sys: 27.3 s, total: 32.9 s

Wall time: 2.08 s

f, ax = plt.subplots(1, figsize=(12, 6))

for i in range(10):

sns.kdeplot(sims[:, i], ax=ax, linewidth=0.1, alpha=0.1, color='k')

plt.show()

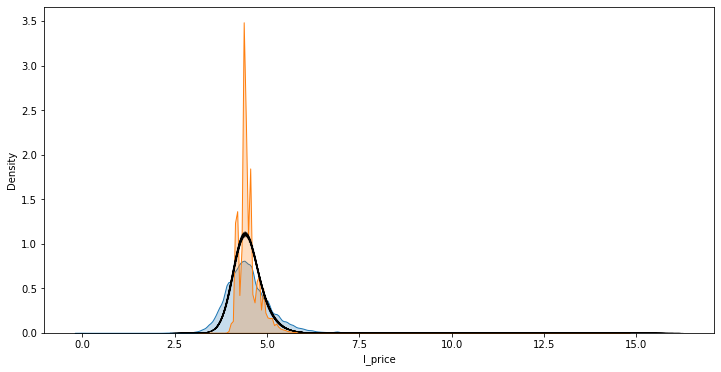

f, ax = plt.subplots(1, figsize=(12, 6))

sns.kdeplot(db['l_price'], shade=True, ax=ax, label='$y$')

sns.kdeplot(m1.fittedvalues, shade=True, ax=ax, label='$\hat{y}$')

for i in range(r):

sns.kdeplot(sims[:, i], ax=ax, linewidth=0.1, alpha=0.1, color='k')

plt.show()

To note:

Black line contains

rthin lines that collectively capture the uncertainty behind the model

New data¶

Imagine we are trying to figure out how much should we charge for a property we want to put on AirBnb.

For example, let’s assume our property is:

new = pandas.Series({'bedrooms': 4,

'bathrooms': 1,

'beds': 8})

%%time

# Parameters

## Number of simulations

r = 2000

# Pull out characteristics for house of interest

x_i = new

# Specify model engine

model = m1

# Place-holder

sims = np.zeros(r)

# Loop over number of replications

for i in range(r):

# Get a random draw of betas

rbs = np.random.normal(model.params, model.bse)

# Get a random draw of epsilon

re = np.random.normal(0, model.scale)

# Obtain point estimate

y_hr = rbs[0] + np.dot(x_i, rbs[1:]) + re

# Store estimate

sims[i] = y_hr

CPU times: user 640 ms, sys: 4.53 ms, total: 644 ms

Wall time: 643 ms

f, ax = plt.subplots(1, figsize=(12, 6))

sns.kdeplot(sims, shade=True, ax=ax, label='Simulation')

ax.axvline(model.params.iloc[0] + np.dot(new, model.params.iloc[1:]), \

c='green', label='Predicted')

lo, up = pandas.Series(sims)\

.sort_values()\

.iloc[[int(np.round(0.025 * r)), int(np.round(0.975 * r))]]

ax.axvline(lo, c='grey', linewidth=1)

ax.axvline(up, c='grey', linewidth=1)

plt.legend()

plt.show()

[Pro]

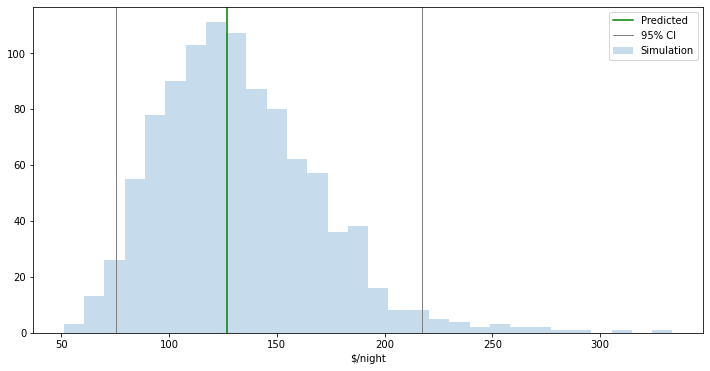

def predictor(bedrooms, bathrooms, beds):

new = pandas.Series({'bedrooms': bedrooms,

'bathrooms': bathrooms,

'beds': beds

})

r = 1000

x_i = new

model = m1

y_hat = model.params.iloc[0] + np.dot(new, model.params.iloc[1:])

# Simulation

sims = np.zeros(r)

for i in range(r):

rbs = np.random.normal(model.params, model.bse)

re = np.random.normal(0, model.scale)

y_hr = rbs[0] + np.dot(x_i, rbs[1:]) + re

sims[i] = y_hr

sims = np.exp(sims)

y_hat = np.exp(y_hat)

# Bands

lo, up = pandas.Series(sims)\

.sort_values()\

.iloc[[int(np.round(0.025 * r)), int(np.round(0.975 * r))]]

# Setup'n'draw figure

f, ax = plt.subplots(1, figsize=(12, 6))

ax.hist(sims, label='Simulation', alpha=0.25, bins=30)

ax.axvline(y_hat, c='green', label='Predicted')

ax.axvline(lo, c='grey', linewidth=1, label='95% CI')

ax.axvline(up, c='grey', linewidth=1)

#ax.set_xlim((0, 10))

# Dress up

ax.set_xlabel("$/night")

plt.legend()

return plt.show()

predictor(3, 1, 1)

# You might have to run this to make interactives work

# jupyter labextension install @jupyter-widgets/jupyterlab-manager

# From https://ipywidgets.readthedocs.io/en/latest/user_install.html#installing-the-jupyterlab-extension

# Then restart Jupyter Lab

from ipywidgets import interact, IntSlider

interact(predictor,

bedrooms=IntSlider(min=1, max=10), \

bathrooms=IntSlider(min=0, max=10), \

beds=IntSlider(min=1, max=20)

);

Model performance¶

To note:

Switch from inference to prediction

Overall idea of summarising model performance

\(R^2\)

Error-based measures

# R^2

r2 = pandas.Series({'Baseline': metrics.r2_score(db['l_price'],

m1.fittedvalues),

'Augmented': metrics.r2_score(db['l_price'],

m3.fittedvalues)})

r2

Baseline 0.244826

Augmented 0.339876

dtype: float64

# MSE

mse = pandas.Series({'Baseline': metrics.mean_squared_error(db['l_price'],

m1.fittedvalues),

'Augmented': metrics.mean_squared_error(db['l_price'],

m3.fittedvalues)})

mse

Baseline 0.271771

Augmented 0.237565

dtype: float64

# MAE

mae = pandas.Series({'Baseline': metrics.mean_absolute_error(db['l_price'],

m1.fittedvalues),

'Augmented': metrics.mean_absolute_error(db['l_price'],

m3.fittedvalues)})

mae

Baseline 0.379119

Augmented 0.357287

dtype: float64

# All

perf = pandas.DataFrame({'MAE': mae,

'MSE': mse,

'R^2': r2})

perf

| MAE | MSE | R^2 | |

|---|---|---|---|

| Baseline | 0.379119 | 0.271771 | 0.244826 |

| Augmented | 0.357287 | 0.237565 | 0.339876 |